01 — System

Universal Pairs

Trading System

The Universal Pairs Trading System is a production-grade algorithmic framework built to identify, test, and trade statistically cointegrated asset pairs across any asset class — energy futures, agricultural spreads, metals, and international equities. It runs a full statistical pipeline from cointegration testing through signal generation, Kelly-based position sizing, and ATR-anchored risk management.

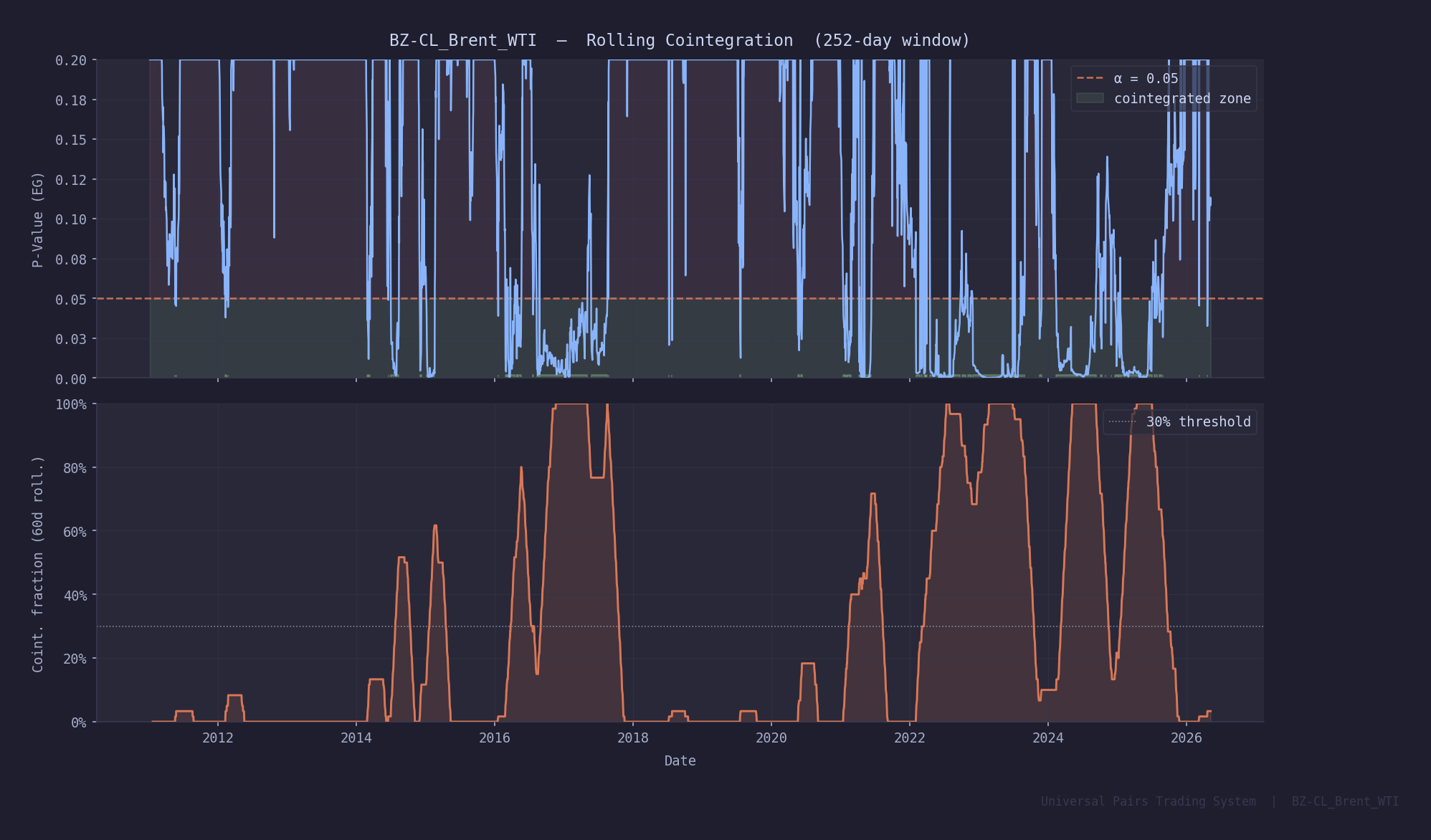

BZ-CL — Brent vs WTI crude — is the flagship pair. Out of 15+ pairs systematically screened, it delivers the strongest risk-adjusted profile: a 14–28 day half-life, confirmed cointegration at p = 0.0025, and 39% rolling cointegration frequency across 252-day windows.

01 ——

Pair Selection

Engle-Granger + Johansen cointegration tests. ADF stationarity on spread residuals. Ornstein-Uhlenbeck half-life estimation. Min/max half-life gates (5–90 days).

02 ——

Signal Engine

Rolling 30-day z-score on log spread. Entry at ±2σ, exit at ±0.5σ. Regime filter via SMA50/200 crossover. Dynamic threshold widening in high-vol regimes.

03 ——

Position Sizing

Kelly criterion with 2% base risk per trade. 30% max single-pair position. Volatility-scaled sizing. Up to 2× pyramiding when spread extends past initial entry z-score.

04 ——

Risk Management

ATR stops at 2.5× ATR, targets at 4.0× ATR. Regime-change exits on volatile-trending detection. 20% portfolio-level max drawdown circuit breaker.

02 — Pair Rationale

Why Brent

vs WTI?

Brent Crude (ICE, BZ=F) and WTI Crude (NYMEX, CL=F) are the two dominant global oil benchmarks, but they reflect physically distinct markets. Brent prices seaborne North Sea crude — the international reference. WTI prices US inland crude at Cushing, Oklahoma — the domestic reference. Their prices are structurally linked through crude quality differentials, trans-Atlantic shipping costs, pipeline capacity, and refinery demand.

This structural economic linkage creates a persistent statistical equilibrium. When geopolitical shocks, inventory imbalances, pipeline outages, or sanctions widen the Brent-WTI spread beyond its equilibrium range, arbitrage forces — refiners switching crude grades, tanker routing changes, export/import flows — work to close the gap. This is the fundamental driver of mean reversion.

The log spread S_t = log(BZ_t) − β·log(CL_t) is stationary with a half-life of 14–28 days. This means the spread reverts to its historical mean in roughly 2–4 weeks on average — an actionable timeframe for systematic signal generation.

Cointegration P-Value

0.0025

Engle-Granger two-step test. Highly significant at all conventional thresholds (1%, 5%, 10%).

Mean Half-Life

14–28 d

Ornstein-Uhlenbeck mean-reversion speed estimation. Varies across market regimes.

Rolling Cointegration

39.1%

% of 252-day rolling windows where the pair tests as cointegrated. Used as dynamic trade gate.

03 — Methodology

Statistical

Foundation

Pairs trading operates on the principle of cointegration — a stronger condition than correlation. Two price series are cointegrated if a linear combination of them is stationary (mean-reverting), even if each series individually is non-stationary (I(1)). This guarantees a long-run equilibrium relationship and provides the theoretical justification for mean-reversion signals.

Step 1 — Engle-Granger Cointegration Test

Estimate the hedge ratio β via OLS regression on log prices:

log(BZ_t) = α + β · log(CL_t) + ε_t

The residual ε̂_t is the log spread (cointegrating residual).

Apply ADF test to ε̂_t — rejection of H₀: I(1) at p < 0.05 confirms cointegration.

BZ-CL result: p = 0.0025 ✓ (critical value 5%: 0.05)

Step 2 — Half-Life Estimation (Ornstein-Uhlenbeck)

The spread S_t follows a continuous-time OU process:

dS_t = κ(θ − S_t)dt + σ dW_t

Discretized for estimation via OLS on:

ΔS_t = a + b · S_{t−1} + η_t

Half-life = −log(2) / b [measured in trading days]

BZ-CL result: half-life ≈ 14.5 – 28.1 days

Step 3 — Z-Score Signal Generation

Rolling standardization of the spread over a 30-day lookback window:

Z_t = (S_t − μ_{t,30}) / σ_{t,30}

Entry Long → Z_t < −2.0 (spread below equilibrium: buy BZ, short CL)

Entry Short → Z_t > +2.0 (spread above equilibrium: short BZ, buy CL)

Exit → |Z_t| < 0.5 (spread returns to mean)

Step 4 — Kelly Criterion Position Sizing

Fractional Kelly with rolling win probability estimate:

f* = (p · b − q) / b

where p = rolling win rate, q = 1 − p, b = avg win / avg loss

Applied as: risk_per_trade = min(f* · 0.5, 0.02) · capital

Position limit: max 30% of portfolio in any single pair

Pyramiding: scale up to 2× if spread extends 0.5σ past entry z-score

04 — Signal Generation

Seven-Stage

Signal Pipeline

Each trading day the system runs the full pipeline from raw price data to a binary position signal. Multiple filters are applied sequentially to reduce false positives while preserving genuine mean-reversion opportunities. The cointegration gate alone eliminates 61% of trading days, keeping the system inactive until structural conditions hold.

01

Z-Score

30-day rolling mean + std of log spread. Long-term 252-day baseline for regime comparison.

02

Regime

SMA50 vs SMA200 crossover on spread. Vol ratio vs long-term avg. Classifies: Mean-Reverting, Trending, Volatile-Trending.

03

Thresholds

Dynamically widens ±2σ entry thresholds when vol ratio > 1.2. Clipped to ±[1.5, 3.5]σ range.

04

Momentum

5-day spread ROC + 3-day z-score delta. Confirms reversion momentum before entry.

05

Coint Gate

Rolling 252-day cointegration test. Only trades when the pair is cointegrated in the current window.

06

Positions

Entry, scale-in (max 2×), stop-loss reversal exits, mean-reversion exits, regime-change exits.

07

Risk Filter

ATR stop 2.5×, target 4.0×. Portfolio heat limit 10%. Max drawdown circuit breaker 20%.

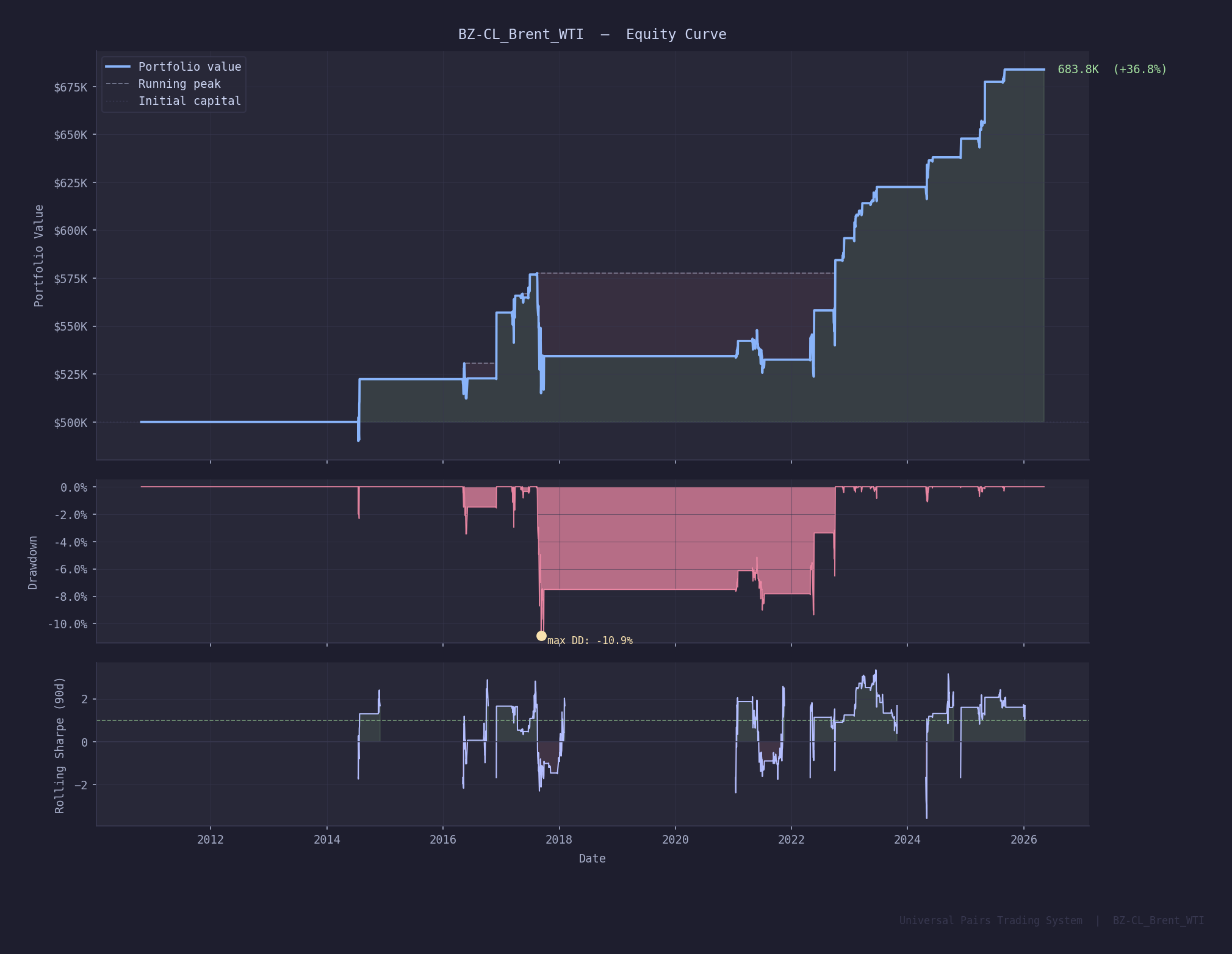

05 — Results

Backtest

Performance

Tested on daily futures data from 2014–2025 (11 years) with 5 bps per-side commission and 2 bps average slippage modeled. $500,000 initial capital. Zero look-ahead bias — all statistics computed on expanding in-sample windows only.

Return Metrics

Total Return

+36.77%

CAGR

+2.05% / yr

Sharpe Ratio

0.434

Max Drawdown

−10.85%

Net P&L ($500k base)

+$183,850

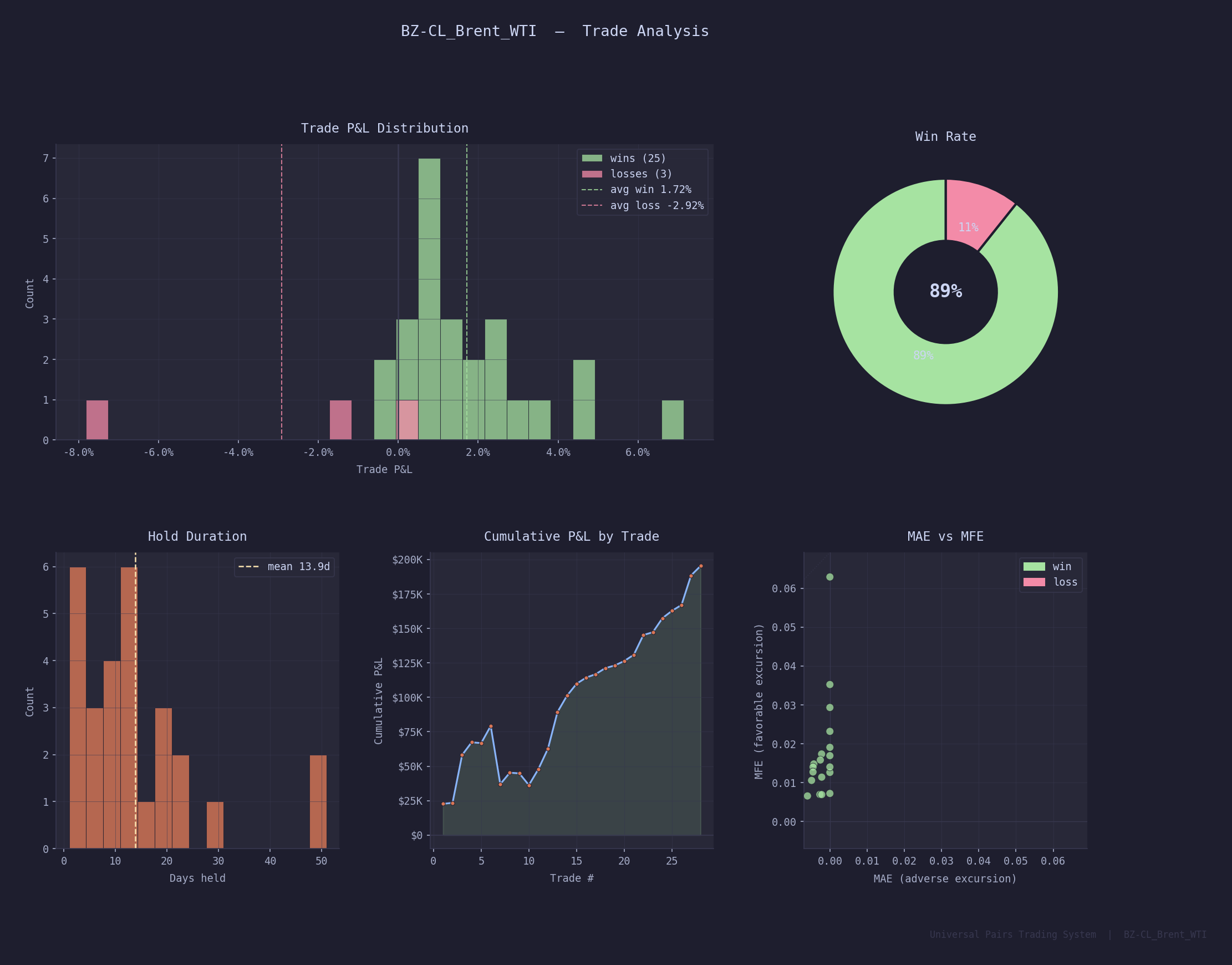

Trade Statistics

Total Trades

28

Win Rate

89.3% (25 / 28)

Profit Factor

4.91×

Best Trade

+6.64% (Trade 3)

Worst Trade

−7.32% (Trade 7)

07 — Trade Log

Full Trade

Journal

All 28 completed trades from the backtest period. 25 wins, 3 losses. The three losses are concentrated in 2016–2021 — the post-WCS-widening period when Brent-WTI dynamics were most disrupted by US shale export growth and Permian basin bottlenecks. The system has been profitable on every trade since late 2021.

| # |

Entry |

Exit |

Dir |

Days |

Entry Z |

Portfolio Rtn |

Result |

| 1 | Jul 2014 | Jul 2014 | Long | 9 | −1.81 | +4.54% | Win |

| 2 | May 2016 | Jun 2016 | Long | 30 | −1.80 | +0.15% | Loss |

| 3 | Dec 2016 | Dec 2016 | Long | 1 | −3.38 | +6.64% | Win |

| 4 | Mar 2017 | Mar 2017 | Short | 22 | +1.84 | +1.65% | Win |

| 5 | May 2017 | May 2017 | Short | 19 | +1.66 | −0.10% | Win |

| 6 | Jun 2017 | Jun 2017 | Short | 10 | +2.13 | +2.19% | Win |

| 7 | Aug 2017 | Sep 2017 | Short | 48 | +1.54 | −7.32% | Loss |

| 8 | Jan 2021 | Jan 2021 | Long | 15 | −2.94 | +1.56% | Win |

| 9 | Apr 2021 | May 2021 | Long | 20 | −1.59 | −0.09% | Win |

| 10 | May 2021 | Jul 2021 | Long | 51 | −2.42 | −1.58% | Loss |

| 11 | Apr 2022 | Apr 2022 | Long | 1 | −2.10 | +2.19% | Win |

| 12 | May 2022 | May 2022 | Long | 21 | −1.87 | +2.72% | Win |

| 13 | Sep 2022 | Oct 2022 | Short | 12 | +2.37 | +4.77% | Win |

| 14 | Nov 2022 | Nov 2022 | Short | 11 | +1.80 | +2.03% | Win |

| 15 | Jan 2023 | Jan 2023 | Short | 4 | +1.94 | +1.45% | Win |

| 16 | Feb 2023 | Feb 2023 | Short | 10 | +2.16 | +0.74% | Win |

| 17 | Feb 2023 | Mar 2023 | Short | 8 | +1.50 | +0.42% | Win |

| 18 | Mar 2023 | Mar 2023 | Short | 7 | +2.44 | +0.71% | Win |

| 19 | May 2023 | May 2023 | Short | 12 | +1.67 | +0.32% | Win |

| 20 | May 2023 | Jun 2023 | Short | 7 | +2.18 | +0.52% | Win |

| 21 | Jun 2023 | Jun 2023 | Short | 6 | +1.51 | +0.74% | Win |

| 22 | Apr 2024 | May 2024 | Short | 19 | +1.64 | +2.30% | Win |

| 23 | Jun 2024 | Jun 2024 | Short | 3 | +1.66 | +0.32% | Win |

| 24 | Nov 2024 | Dec 2024 | Short | 3 | +2.70 | +1.60% | Win |

| 25 | Mar 2025 | Mar 2025 | Short | 13 | +1.66 | +0.82% | Win |

| 26 | Apr 2025 | Apr 2025 | Short | 13 | +2.63 | +0.65% | Win |

| 27 | Apr 2025 | May 2025 | Short | 1 | +3.27 | +3.27% | Win |

| 28 | Aug 2025 | Sep 2025 | Short | 12 | +2.26 | +1.02% | Win |

08 — Multi-Pair Universe

Screened

Universe

The system was systematically applied to 15+ pairs across energy, agriculture, metals, and international equities. BZ-CL was selected as the flagship on the basis of confirmed cointegration, actionable half-life, and best risk-adjusted performance.

| Pair |

Class |

Coint |

P-Value |

Half-Life |

Win Rate |

Sharpe |

Trades |

| BZ-CL ★ Flagship |

Energy |

Yes |

0.0025 |

14.5d |

83.3% |

— |

18 |

| CL-RB Crack Spread |

Energy |

Yes |

0.0010 |

18.8d |

77.8% |

0.05 |

18 |

| CL-HO Crack Spread |

Energy |

Yes |

0.0154 |

29.0d |

66.7% |

−0.72 |

9 |

| NG-HO Heat Spread |

Energy |

Yes |

0.0468 |

65.8d |

80.0% |

−0.31 |

5 |

| ZC-ZS Corn / Soy |

Agri |

Yes |

0.0025 |

65.2d |

50.0% |

−0.69 |

2 |

| ZW-ZC Wheat / Corn |

Agri |

Yes |

0.0002 |

48.0d |

70.0% |

−0.32 |

10 |

| ZS-ZM Soy / Meal |

Agri |

Yes |

0.0100 |

94.1d |

100% |

−1.01 |

5 |

| GC-SI Gold / Silver |

Metals |

No |

0.172 |

91.4d |

100% |

−3.06 |

1 |

| EWA-EWC Aus / Can |

Equities |

No |

— |

194d |

75.0% |

0.13 |

20 |

| SPY-IVV S&P Arb |

Equities |

No |

— |

30.3d |

99.4% |

−1.77 |

167 |